California Warranty Deed Overview

California has its own distinct real estate culture, and warranty deeds are not the dominant instrument here. Most California residential transactions use a grant deed, which carries statutory implied covenants under Civil Code Section 1113 but does not provide the full title guarantee of a general warranty deed. That said, warranty deeds are legally valid in California and are sometimes used in commercial transactions or when a buyer specifically negotiates for stronger title covenants. If you are recording a warranty deed in California, the process runs through the county recorder's office in the county where the property is located.

California's Documentary Transfer Tax starts at $1.10 per $1,000 of consideration at the county level, but many cities and counties impose additional local transfer taxes that can significantly increase this amount. Recording fees begin at $15 for the first page. A Preliminary Change of Ownership Report must accompany the deed at recording. Proposition 13 makes the reassessment question a major financial concern in California transfers, as properties held for decades can have assessed values far below current market value, and a transfer triggers reassessment unless an exclusion applies.

$15

Recording fee

$1.10 per $1,000

Transfer tax

Required

Notarization

0

Witnesses required

California Requirements

California county recorders have specific formatting requirements including minimum font sizes, margin widths, and a blank area at the top right of the first page reserved for the recorder's use. A Preliminary Change of Ownership Report is mandatory and must accompany the deed or the recorder will either reject the filing or record it with a penalty surcharge.

California Specific Note

A Preliminary Change of Ownership Report must accompany your deed at recording, or the recorder will charge a penalty fee or reject the document. The state Documentary Transfer Tax is $1.10 per $1,000, but many California cities and counties impose additional local transfer taxes that can be several times higher, particularly in the Bay Area and Los Angeles. The Proposition 13 reassessment rules mean that a deed transfer can substantially increase annual property taxes unless an exclusion applies. File a claim for any applicable exclusion with the county assessor promptly after recording.

Document Requirements

- Notarization: Must be notarized by a California notary public or authorized notary

- Witnesses: California requires 0 additional witness(es)

- Legal Description: Complete legal description as it appears on the current deed of record

- Parcel Number: Assessor's parcel number or tax ID

- Return Address: Mailing address for returning the recorded document

- Formatting: Standard formatting with adequate margins, black ink, minimum 10-point font

How to File in California

California has several steps beyond basic execution and recording, including the mandatory PCOR and the Documentary Transfer Tax calculation. Work through each step carefully to avoid delays at the recorder's window.

Prepare the Deed

Complete all fields: grantor and grantee legal names, the full legal description from the prior deed, the assessor's parcel number, and the consideration amount. Leave the required blank space in the upper right corner of the first page for the recorder's stamp. Note the Documentary Transfer Tax amount on the face of the deed or on a separate page, showing the calculation.

Complete the Preliminary Change of Ownership Report

Download the PCOR form from the county assessor's website or pick one up at the recorder's office. The transferee completes it. The form asks about the nature of the transfer, the purchase price, financing terms, and whether any Proposition 13 reassessment exclusions are being claimed. Filing an inaccurate PCOR can affect the reassessment outcome.

Get the Deed Notarized

The grantor signs before a California notary public, who uses the form of acknowledgment prescribed by California Government Code 1189. Bring a California driver's license or other acceptable ID. California notary fees are capped at $15 per signature by statute. Remote online notarization is permitted in California but confirm the county recorder accepts RON-acknowledged documents before using that method.

Submit to the County Recorder with the PCOR

Submit the executed deed and the completed PCOR together to the county recorder's office. Most California county recorders accept e-recording and many accept mail filings. Pay the recording fee (starting at $15 per document) and the Documentary Transfer Tax at the same time. In high-tax cities, confirm the local city transfer tax amount before filing, as some cities collect separately.

File for Any Reassessment Exclusion

If the transfer qualifies for a Proposition 13 reassessment exclusion, such as a parent-to-child transfer under Proposition 19, file the claim form with the county assessor promptly. Deadlines apply, and missing them means a reassessment at current market value, which for properties held long-term can substantially increase annual property taxes.

California Fees & Costs

Typical costs for filing in California. Actual fees may vary by county.

| Fee / Tax | Amount |

|---|---|

| Recording Fee | $15 |

| Transfer Tax | $1.10 per $1,000 |

| Notarization | $5 - $25 per signature |

| Certified Copy | $1 - $10 per page |

| Attorney Review (optional) | $150 - $500 |

California Tax Implications

California's tax picture for property transfers is genuinely complex compared to most states. The Documentary Transfer Tax at the county level is $1.10 per $1,000 of consideration, but that is often just the starting point. Cities like San Francisco impose their own transfer taxes ranging from 0.5% to 3% based on sale price. Los Angeles, Santa Monica, and Culver City have added transfer taxes in recent years at high rates on properties above certain thresholds. For a $2 million San Francisco property, the combined transfer tax can exceed $60,000. Know the full local tax stack before closing.

Proposition 13 is the defining property tax issue for California deed transfers. It limits the taxable assessed value to the 1978 purchase price adjusted by no more than 2% per year. A property bought for $80,000 in 1980 might be assessed at just $150,000 today, while a neighbor's identical house sells for $1.5 million. When ownership transfers, the county assessor reassesses the property to current market value. For long-held properties in high-appreciation markets, this can increase annual property taxes by $15,000 or more. Proposition 19, which took effect in February 2021, significantly narrowed the parent-child reassessment exclusion that previously allowed most transfers between parents and children to avoid reassessment. Under current rules, the exclusion only applies if the child makes the property their primary residence, and even then only shelters a portion of the value.

California also has a state income tax on capital gains treated as ordinary income, with a top rate of 13.3%. Unlike some states that offer a preferential capital gains rate, California taxes capital gains at the same rate as other income. For a seller who purchased their California home for $300,000 and sells for $1.5 million, the federal and California combined tax on the gain, after the primary residence exclusion, can be substantial. Consult a California CPA before structuring any transfer where capital gains exposure is a factor.

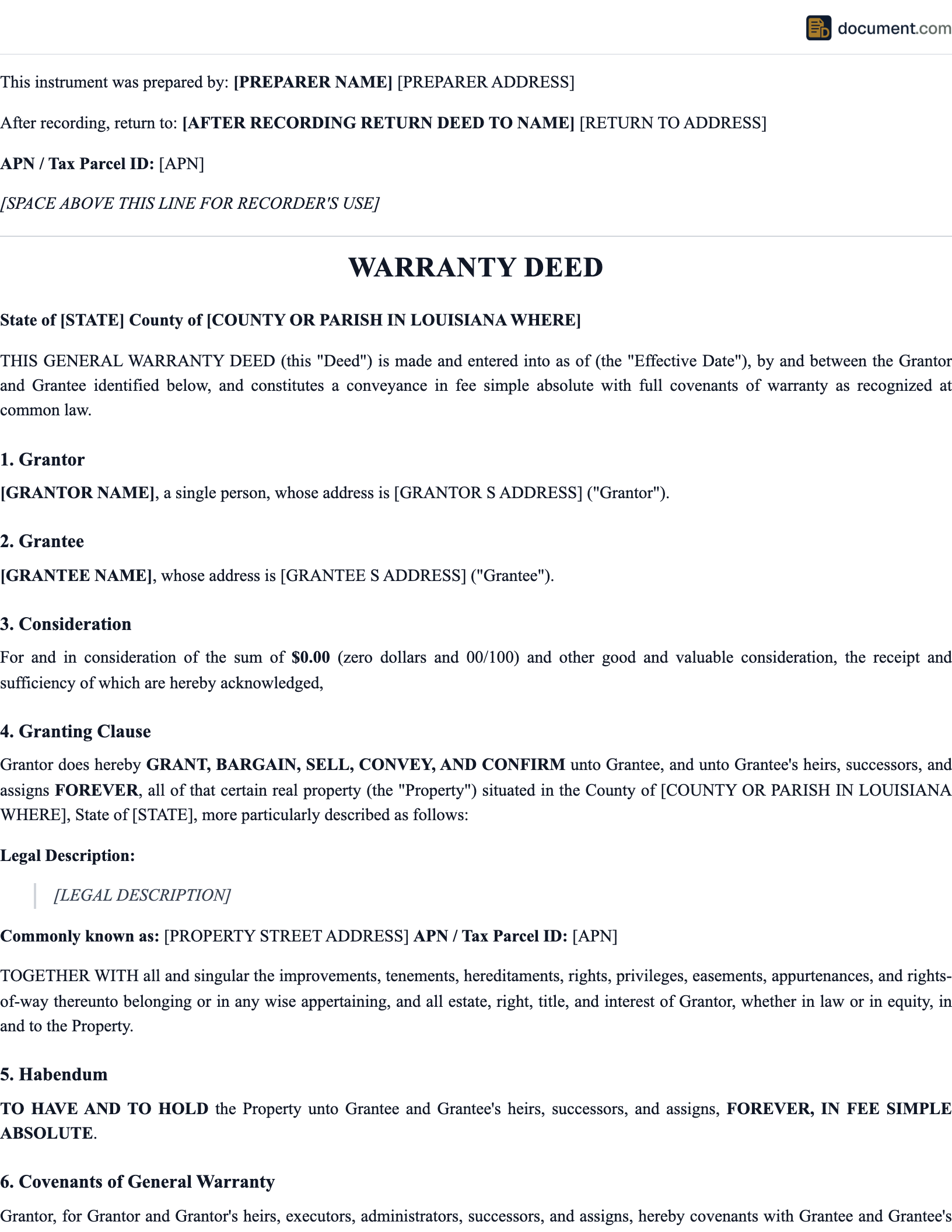

Sample California Warranty Deed

Preview of our California-specific template. Your document will include all fields required for recording in any California county.

WARRANTY DEED (GENERAL WARRANTY DEED)

STATE OF CALIFORNIA

Legal Document

PARTY INFORMATION

Name: [Full Legal Name]

Address: [California Address]

County: [County]

PROPERTY DESCRIPTION

County: [County] State: California

Legal Description: [Per Recorded Plat]

Parcel No.: [APN]

California Warranty Deed FAQ

Common questions about filing in California, including requirements, fees, and tax implications.

Official California Resources

Official state resources for verifying requirements and finding your local recording office.

Important Considerations

The Proposition 13 reassessment question should be the first thing you analyze for any California property transfer. If the property has been held for twenty or thirty years in an appreciating market, the tax increase from reassessment can dwarf every other cost in the transaction. Understand upfront whether any exclusion applies, what the deadlines are to claim it, and what the property will be taxed on after the transfer.

Community property law applies in California, just as it does in Arizona. Property acquired by a married person during marriage is presumed community property. Both spouses must sign a deed conveying community property, even if title is held in only one name. Failure to obtain both signatures can leave the non-signing spouse's interest outstanding, which will create a title defect at the next transfer.

California is an escrow state for most residential transactions, meaning closings are handled by a licensed escrow company or attorney acting as escrow, not a title company acting as closing agent as in many East Coast states. The escrow officer coordinates the deed recording, collection and payment of transfer taxes, payoff of existing liens, and distribution of proceeds. For transactions handled through escrow, the escrow officer will typically manage the recording process, but you should still verify that the correct transfer taxes have been calculated, including any local city taxes that might be missed.

The PCOR is not optional and is not a formality. The county assessor uses it to determine how to classify the transfer and whether reassessment is triggered. Filling it out inaccurately, particularly about whether consideration was paid or whether a family relationship exists, can result in incorrect assessments that are difficult to correct after the fact.

California Prop 13 Note

For transfers between parents and children, the Proposition 19 rules that took effect in February 2021 changed the exclusion significantly compared to prior law. The child must move into the property as their primary residence within one year, and the exclusion only applies to the difference between the assessed value and the current value up to $1 million above the assessed value. Properties that exceed this threshold will be partially reassessed. Consult a California estate planning or real estate attorney before relying on a parent-child exclusion under Prop 19.

Related Documents

Depending on your situation, you may need additional documents alongside this one. Below are commonly related documents that are frequently used together in real estate transactions.

Important Considerations

California residential real estate transactions almost universally use title and escrow companies to coordinate closing and recording. If you are handling a deed transfer outside of a traditional sale, such as a gift, an estate distribution, or a family transfer, you can record directly with the county recorder, but you still need to submit the PCOR and calculate the Documentary Transfer Tax correctly. Missing the PCOR will result in either a rejection or a penalty surcharge.

Proposition 13 is the most consequential financial factor in California property transfers after the purchase price itself. For a property purchased in the 1980s or 1990s in a coastal market, the tax increase from reassessment can be $15,000 to $30,000 per year or more. Before transferring property to an adult child or another family member, fully analyze whether a Proposition 19 exclusion is available, what steps must be taken to qualify, and what the post-transfer tax bill will look like with and without the exclusion.

Community property rules in California require both spouses to sign when conveying community property. California also recognizes community property with right of survivorship as a form of vesting. Review the current title vesting carefully before preparing the deed to confirm whose signature is needed.

Local transfer taxes in California cities can be substantial and are sometimes overlooked in initial closing cost estimates. San Francisco, Los Angeles, Oakland, Santa Monica, and other cities all have their own transfer tax ordinances with varying rates and thresholds. Confirm whether a city transfer tax applies and whether it is paid by the buyer, seller, or split between them, as local practice varies.

California Prop 19 Note

Proposition 19 dramatically changed the rules for parent-to-child and grandparent-to-grandchild property transfers effective February 16, 2021. The old blanket exclusion that let parents transfer any property to children without reassessment is gone. The new exclusion is narrower, applies only to a primary residence, and only shelters up to $1 million of value above the current assessed value. For high-value properties, partial reassessment is now the norm even for qualifying transfers. Consult a California estate planning attorney before structuring any intergenerational transfer.

Related Documents

Depending on your situation, you may need additional documents alongside this one. Below are commonly related documents that are frequently used together in real estate transactions.

Create your California Warranty Deed in under 5 minutes.

Answer a few questions and download a California-compliant document, ready for the state agency.