What Is a Hold Harmless Agreement?

A hold harmless agreement — also called an indemnity agreement, indemnification clause, or hold-harmless clause — is a contract provision in which one party (the indemnitor) agrees to assume legal liability for losses, claims, or damages that would otherwise fall on another party (the indemnitee). The function of the agreement is to shift risk from the party most likely to be sued to the party best positioned to control or insure against the underlying hazard. Hold harmless clauses appear in nearly every commercial contract: construction subcontracts, equipment rentals, lease agreements, service agreements, recreational activity waivers, and event venue contracts. They are one of the most heavily negotiated provisions in any contract because they directly determine who bears the cost when something goes wrong.

Although "hold harmless" and "indemnify" are often used interchangeably, they have technically different meanings. To indemnify is to reimburse another party for a loss already incurred — a backward-looking duty to make someone whole. To hold harmlessis to assume the legal liability in the first place so the protected party never bears the loss at all — a forward-looking duty to absorb the risk. Most modern agreements pair the two with the phrase "indemnify, defend, and hold harmless," which creates three distinct obligations: providing legal defense, paying judgments and settlements, and accepting liability outright. Courts in some states treat the words as synonymous; others have ruled that "hold harmless" provides meaningfully broader protection.

Hold harmless agreements are categorized by how much risk the indemnitor accepts. A limited form (Type I)indemnity makes the indemnitor responsible only for losses caused by the indemnitor's own negligence. An intermediate form (Type II)indemnity covers all losses except those caused solely by the indemnitee's negligence. A broad form (Type III) indemnity holds the indemnitor liable for everything, including losses caused entirely by the indemnitee. Broad form indemnity is the most aggressive type and is increasingly unenforceable in many states, particularly in the construction industry, where legislatures have enacted anti-indemnity statutes to prevent powerful contractors from forcing weaker subcontractors to accept liability for accidents the contractor caused.

The legal enforceability of a hold harmless agreement depends on multiple factors. Courts strictly construe indemnity provisions against the party seeking protection, meaning any ambiguity is resolved in favor of the party giving up rights. To be enforceable, the clause must be clear and conspicuous, supported by valid consideration, signed by parties with authority to bind their organizations, and consistent with public policy and applicable statutes. Courts will not enforce hold harmless provisions that purport to cover gross negligence, willful misconduct, intentional torts, fraud, or criminal acts — these categories of conduct are off-limits regardless of how the contract is drafted.

A hold harmless promise is only as valuable as the indemnitor's ability to pay. For this reason, well-drafted agreements are almost always backed by mandatory insurance requirements. The indemnitor must maintain commercial general liability insurance, often with $1 million per occurrence and $2 million aggregate minimums; automobile liability coverage; workers' compensation as required by law; and umbrella or excess liability policies for higher-risk activities. The indemnified party is typically named as an additional insured on the indemnitor's policies, certificates of insurance are exchanged before work begins, and a waiver of subrogation is included to prevent the insurer from later pursuing the indemnified party.

Risk Allocation

Clearly assign liability to the party best positioned to manage and insure the risk

Insurance Backed

Pair the promise with mandatory coverage so the indemnitor can actually pay claims

State Compliant

Drafted to comply with anti-indemnity statutes in construction and other regulated industries

Hold Harmless Agreement Form Preview

Below is a structured preview of the sections included in a standard hold harmless and indemnity agreement. Your final document will be tailored to your specific transaction, state law requirements, and the level of risk transfer appropriate for the relationship.

HOLD HARMLESS AND INDEMNITY AGREEMENT

Risk Transfer and Indemnification

INDEMNITOR (Party Assuming Liability)

Name / Entity: [Legal Name]

Address: [Street, City, State, ZIP]

Type: [Individual / LLC / Corporation]

INDEMNITEE (Party Being Protected)

Name / Entity: [Legal Name]

Address: [Street, City, State, ZIP]

UNDERLYING ACTIVITY OR TRANSACTION

Description: [Construction project, services, equipment use, event, etc.]

Location: [Site / Address]

Effective Dates: [Start - End]

SCOPE OF INDEMNITY

Form: [Limited (Type I) / Intermediate (Type II) / Broad (Type III)]

Covered Claims: [Bodily injury, property damage, third-party claims, etc.]

Carve-Outs: [Gross negligence, willful misconduct]

DUTY TO DEFEND

Defense Obligation: [Provide counsel of indemnitee's choosing / mutual selection]

Defense Costs: [Indemnitor pays all reasonable fees and costs]

INSURANCE REQUIREMENTS

Commercial General Liability: $[1,000,000] per occurrence

Aggregate Limit: $[2,000,000]

Auto Liability: $[1,000,000]

Workers' Comp: [Statutory limits]

Additional Insured: [Indemnitee named on policy]

SURVIVAL & TERMINATION

Survival Period: [Statute of limitations / repose]

Termination Trigger: [Completion / Mutual agreement]

GOVERNING LAW & SIGNATURES

Governing Law: State of [State]

Indemnitor Signature: [Signature Line]

Indemnitee Signature: [Signature Line]

Date: [Execution Date]

Types of Hold Harmless Clauses

Hold harmless clauses are categorized first by who is protected (unilateral or reciprocal) and second by how broadly liability is shifted (limited, intermediate, or broad form). Choosing the right type is critical because the wrong choice may be either unenforceable or grossly unfair, depending on the relationship.

Hold Harmless vs Indemnification vs Waiver

Hold harmless agreements are often confused with related risk-shifting documents. Each serves a different legal function and uses different language. Understanding the distinctions helps you choose — or combine — the right instruments.

| Feature | Hold Harmless | Indemnification | Liability Waiver |

|---|---|---|---|

| Function | Assumes liability outright | Reimburses losses after the fact | Releases the right to sue |

| Direction | Forward-looking | Backward-looking | Forward-looking |

| Third-party claims | Yes — primary use | Yes | No — only between signing parties |

| Common context | Construction, services, leases | Commercial contracts, M&A | Recreation, events, fitness |

| Defense duty included? | Often yes (when paired with "defend") | Sometimes | No |

| Statutory limits | Anti-indemnity laws | Anti-indemnity laws | Public policy + minor rules |

How to Create a Hold Harmless Agreement

A defensible hold harmless agreement requires careful drafting and the right state-specific language. Follow these steps to create one that will stand up in court.

Identify the parties

Use the full legal name and address for each party. Identify whether the party is an individual, sole proprietor, partnership, LLC, or corporation. Confirm that the signatory has authority to bind the entity.

Describe the underlying activity

Specifically describe the work, transaction, or activity giving rise to the indemnity. Vague descriptions like 'work performed' invite disputes about scope. Identify the location, dates, and nature of the activity.

Choose the form (Type I, II, or III)

Decide whether the indemnitor accepts only its own negligence (Type I), all losses except the indemnitee's sole negligence (Type II), or every loss including the indemnitee's own negligence (Type III). Check your state's anti-indemnity statute first.

Spell out covered claims

List the categories of claims covered: bodily injury, property damage, economic loss, third-party claims, attorney's fees, defense costs. The broader you draft this list, the more clearly it must align with the chosen form.

Carve out gross negligence and willful misconduct

Expressly exclude gross negligence, willful misconduct, intentional acts, fraud, and criminal acts. Most states will not enforce indemnity for these anyway, and excluding them protects the rest of the clause from being struck down.

Add a duty to defend

If you want defense costs covered, expressly include the duty to defend. Specify whether the indemnitor controls counsel selection, whether the indemnitee can choose its own counsel, and how disputes about defense are resolved.

Require insurance

Mandate commercial general liability, automobile, workers' compensation, and umbrella coverage with specific minimum limits. Require additional insured status, waiver of subrogation, and certificates of insurance before work begins.

Add survival language

State that the indemnity obligations survive termination, expiration, or completion of the underlying contract for the duration of any applicable statute of limitations or repose.

Specify governing law

Choose the law that will govern the agreement. Anti-indemnity statutes apply based on the project location, not the choice-of-law clause, so check both jurisdictions.

Sign with authority

Have authorized representatives sign for each party. For high-value agreements, include corporate resolutions or signature authority documentation.

Key Components

Every enforceable hold harmless agreement contains a core set of provisions. Missing any one of these can render the agreement ambiguous or unenforceable.

Identification of parties

Clear designation of indemnitor and indemnitee, with full legal names.

Recitals

Background explaining the relationship and the activity at issue.

Indemnity grant

Operative language assuming liability and the duty to hold harmless.

Scope and exclusions

What claims are covered and what is carved out.

Defense obligation

Duty to provide and pay for legal defense of covered claims.

Insurance requirements

Mandatory coverage types, limits, and additional insured status.

Survival clause

Indemnity obligations continue after the contract ends.

Governing law and venue

Which state's law applies and where disputes are resolved.

Anti-Indemnity Statutes

Anti-indemnity statutes are state laws that prohibit certain types of indemnity clauses, primarily in construction contracts. They were enacted because legislatures concluded that powerful general contractors and project owners were forcing weaker subcontractors to assume liability for accidents the indemnitee caused — an unfair allocation of risk that distorted incentives for safety and pushed costs onto parties least able to bear them.

More than 40 states currently have anti-indemnity statutes covering construction. The scope of these laws varies widely. Some states only void broad form (Type III) indemnity, allowing intermediate (Type II) clauses to stand. Others void anything beyond limited (Type I) indemnity. A few states extend their protections beyond construction to oilfield services, motor carriers, design professionals, and even general commercial contracts. Choice-of-law clauses cannot be used to circumvent anti-indemnity statutes — most states apply their own statute regardless of what law the contract says governs.

The most aggressive anti-indemnity states include California (which voids any indemnity for the indemnitee's active negligence in construction), Texas (which has detailed rules on additional insured status and indemnity in construction), New York (where General Obligations Law §5-322.1 voids broad and intermediate indemnity in construction), and Illinois (which voids any indemnity for the indemnitee's own negligence in construction). Always check the current statute in the state where the work is performed before relying on a hold harmless clause.

Insurance Backing for Hold Harmless

A hold harmless promise from a party with no money is worthless. The most important practical feature of a hold harmless agreement is the insurance that backs it up. A judgment-proof indemnitor cannot pay claims, no matter how clearly the contract assigns liability. For this reason, every well-drafted hold harmless clause includes mandatory insurance requirements.

Commercial General Liability (CGL)

Standard requirement of $1M per occurrence and $2M aggregate. Covers bodily injury, property damage, and personal/advertising injury.

Automobile Liability

Required when work involves vehicles. Typically $1M combined single limit covering owned, hired, and non-owned autos.

Workers' Compensation

Required by statute in nearly every state when the indemnitor has employees. Statutory limits plus employer's liability.

Umbrella / Excess Liability

Additional layer of $1M-$25M+ over the underlying CGL and auto policies. Common for higher-risk projects.

Professional Liability (E&O)

Required for design professionals, consultants, and other knowledge-based services. Typically $1M-$5M per claim.

Pollution Liability

Required for environmental, demolition, or contaminated-site work. Excluded from standard CGL policies.

Legal Requirements

Hold harmless agreements must satisfy basic contract formation requirements (offer, acceptance, consideration, capacity, mutual assent), plus several additional standards unique to indemnity provisions. Courts apply heightened scrutiny because these clauses shift legal liability away from the party that would otherwise bear it.

Clear and conspicuous

Indemnity language must be plainly visible — not buried in fine print or boilerplate.

Specific and unambiguous

Courts construe ambiguities against the indemnitee. Generic language fails.

Consideration

Each party must give something of value. Continued business is usually sufficient.

Public policy compliant

Cannot waive liability for gross negligence, willful misconduct, or intentional torts.

Statutory compliance

Must satisfy anti-indemnity statutes in the project's jurisdiction.

Authority to sign

Signatory must have actual or apparent authority to bind the entity.

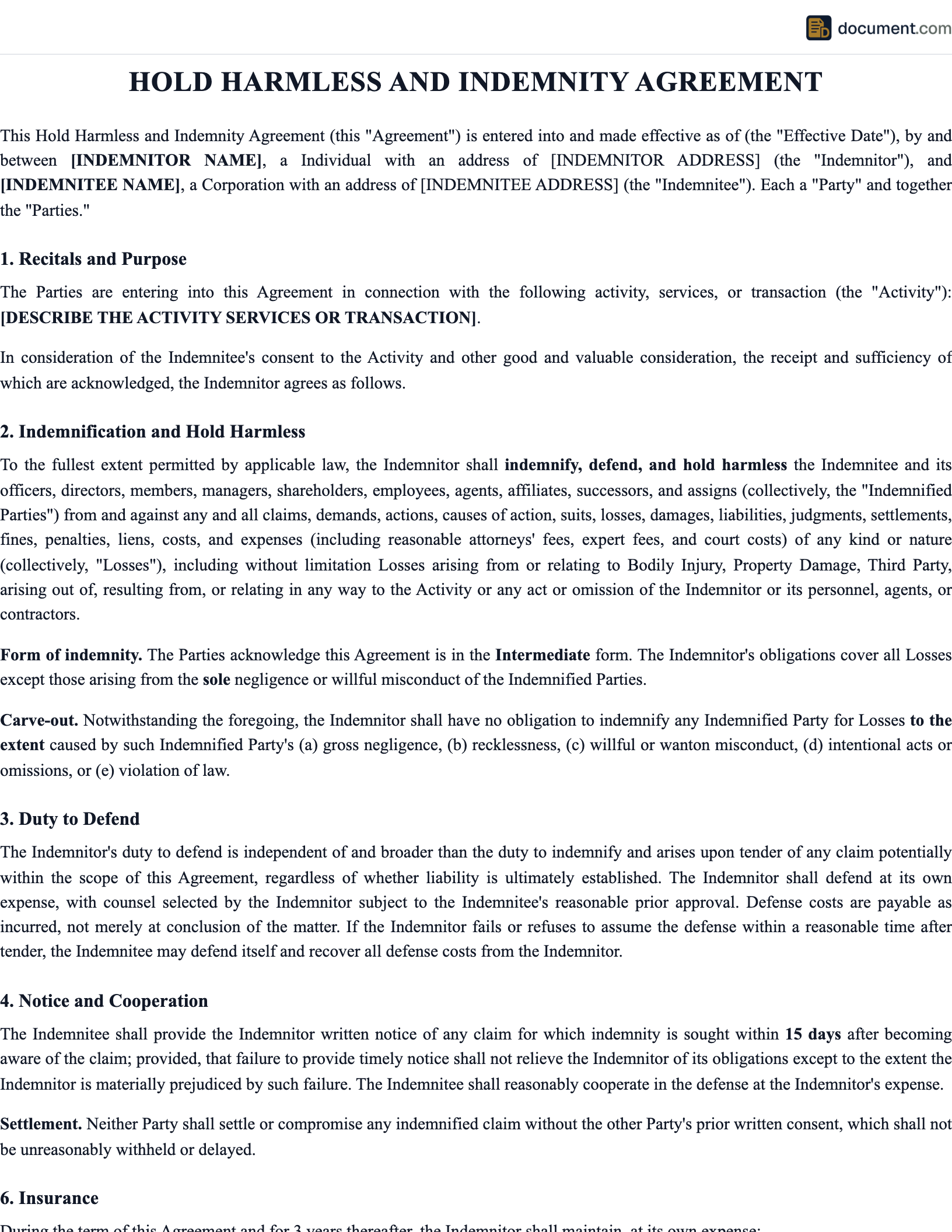

Sample Hold Harmless Agreement

Below is a representative excerpt of the operative language in a hold harmless and indemnity agreement. Your final document will include state-specific compliance language and the full set of operative provisions.

HOLD HARMLESS AND INDEMNITY AGREEMENT

This Hold Harmless and Indemnity Agreement ("Agreement") is made and entered into as of [DATE], by and between [INDEMNITOR NAME]("Indemnitor") and [INDEMNITEE NAME]("Indemnitee").

1. INDEMNIFICATION.To the fullest extent permitted by law, Indemnitor shall indemnify, defend, and hold harmless Indemnitee from and against any and all claims, demands, suits, judgments, losses, liabilities, damages, costs, and expenses (including reasonable attorneys' fees) of every kind arising out of or in any way connected with the activities described herein, except to the extent caused by the sole negligence or willful misconduct of Indemnitee.

2. DUTY TO DEFEND. Indemnitor shall, at its own cost and expense, defend any and all claims or actions covered by this Agreement using counsel reasonably acceptable to Indemnitee.

3. INSURANCE. Indemnitor shall maintain commercial general liability insurance with limits of not less than $1,000,000 per occurrence and $2,000,000 aggregate, naming Indemnitee as an additional insured on a primary and non-contributory basis, with a waiver of subrogation in favor of Indemnitee.

4. SURVIVAL. The obligations under this Agreement shall survive the completion or termination of the underlying activity for the duration of the applicable statute of limitations and repose.

5. EXCLUSIONS.This Agreement does not require Indemnitor to indemnify Indemnitee for losses caused by Indemnitee's gross negligence, willful misconduct, intentional acts, fraud, or criminal conduct.

6. GOVERNING LAW. This Agreement shall be governed by and construed under the laws of the State of [STATE], without regard to its conflict-of-law principles.

Indemnitor Signature

Name: _______________

Date: _______________

Indemnitee Signature

Name: _______________

Date: _______________

Frequently Asked Questions

Answers to the most common questions about hold harmless and indemnity agreements, enforceability, anti-indemnity statutes, and insurance requirements.

Official Resources

Trusted government and industry resources for additional information on indemnity, insurance, and risk management.

OSHA — Construction Safety

Federal workplace safety standards relevant to indemnity in construction

National Association of Insurance Commissioners

Insurance regulation and consumer guidance for liability coverage

ABA Forum on Construction Law

Resources on indemnity and risk allocation in construction contracts

International Risk Management Institute

Industry-leading guidance on additional insured endorsements and indemnity

Create your Hold Harmless Indemnity Agreement in under 10 minutes.

Answer a few questions and download a compliant, attorney-drafted document ready for your state.